KUALA LUMPUR: The spate of lower earnings reported by Hai-O Enterprise Bhd has prompted questions on the viability of the multi-level marketing (MLM) model following amendments to the Direct Selling Act (DSA). In addition, the possible slowdown in consumer spending due to heightening inflation pressure does not help too.

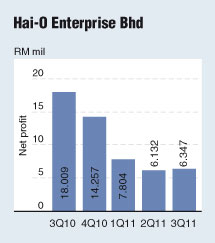

Last week, Hai-O announced that its net profit for its third quarter ended Jan 31, 2011 (3QFY11) plunged 63.76% to RM6.35 million from RM18 million a year ago while revenue halved to RM57.62 million.

The company attributed its dismal results to its MLM division that has suffered from lower contributions for the past three quarters.

In 3QFY11, Hai-O’s MLM business contributed over 55% of its revenue, which according to OSK Research was lower than the division’s historical contribution of over 70%.

For the nine months, Hai-O’s net profit halved to RM20.28 million from RM56.66 million while revenue fell 60% to RM164.99 million from RM412.23 million a year ago.

So, has the MLM model run its course? Not necessarily, said an analyst with RHB Research, as the success of MLM, like other retail businesses, depends to a large degree on the range of products on offer.

“Selling via the MLM business model is alright provided you have strong products to back it. The products have to be something that people want, something usable,” he said.

OSK Research noted that Hai-O’s Malaysia MLM division has seen some improvements while its Indonesian MLM sales too have started to pick up. Its analyst believed that it would take some time for Hai-O to ramp up its MLM business in Indonesia as the country was not an easy market.

Moving forward, Hai-O said its MLM division would continue to broaden its product range, organise more training workshops and launch more effective sales campaign for distributors.

Hai-O also said its wholesale and retail divisions are taking proactive measures to strengthen its existing network and open more outlets at strategic locations in view of the slowing domestic growth.

According to Hai-O, the larger revenue decrease from its MLM division had offset higher revenue contributions from its wholesale and retail divisions in 3QFY11.

The company’s wholesale and retail segments generated over 20% each to the group’s sales, with its retail business boosted by strong sales during the Chinese New Year season.

RHB Research’s analyst said the growth in Hai-O’s retail and wholesale businesses was likely because those were currently at a low base, but were unlikely to overtake MLM as a key earnings driver in the near term.

“Yes, Hai-O’s retail business is growing but it still depends on walk-in customers who are familiar with the brand. In a sense, the retail part of Hai-O is also driven by its membership,” said the analyst.

OSK Research anticipates Hai-O’s earnings to be RM27.2 million and RM32.2 million for FY11 and FY12, respectively.

In a recent note, RHB Research said it continued to be cautious on Hai-O’s MLM division despite a slight growth quarter-on-quarter in MLM revenue of 8.6% to RM29 million in 3QFY11.

Hai-O’s membership recruitment drive and the growth momentum of its base could continue to be impacted from internal restructuring of its MLM division due to the recent amendments in the DSA, RHB Research said.

RHB Research ceased coverage of the company while maintaining its underperform call on Hai-O’s stock with a fair value of RM1.35.

“Hai-O needs to reinvent itself by moving away from its existing product mix to generate a new, more sustainable earnings stream in order to excite investors again in the medium term,” said RHB Research.

Hai-O’s range of MLM products includes its stable of Chinese medicine and health products, as well as items like water filtration systems, lingerie and personal care products.

“In view of the current skittish and volatile market environment, we believe investors are looking for more earnings stability and reliable returns, which Hai-O would not be able to offer at this juncture, in our opinion,” the research house said.

For investors wanting exposure in the MLM sector, RHB Research instead recommended Amway (Malaysia) Holdings Bhd. Ascribing a fair value of RM9.35, the research house preferred Amway for its strong dividend yield of 6% to 7% and stable earnings outlook.

Previously a darling stock, Hai-O shares were on a steady decline from its all-time high of RM4.58 on April 9 last year to an 18-month low of RM2.17 on March 24. It closed at RM2.20 last Friday.

Conversely, Amway shares have been climbing to hit a historic high of RM8.70 last Friday.

Analysts said Amway’s performance had outshone its competitors due to its strong branding, presence and wide range of products covering home appliances, costume jewellery, nutrition products, food and beverages and home living products.

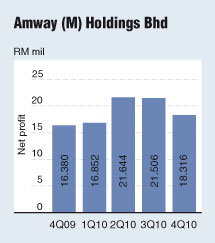

For FY10 ended Dec 31, Amway’s net profit grew 8.11% to RM78.32 million from RM72.44 million while revenue rose 8.36% to RM719.41 million from RM663.9 million a year ago.

Amway, which expects single-digit growth in sales revenue this year, said sales growth in FY10 was mainly driven by the increase in distributors’ productivity from the sales and marketing programmes and distributor price increase, among other factors.

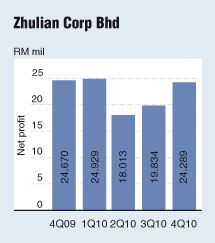

Analysts also cite Zhulian Corp Bhd’s MLM business to underscore the importance of having a strong member base and good product mix, Zhulian has a strong rural base and there is demand for its products, which are affordable and have a high turnover, said one analyst.

Zhulian is known for its jewellery products, but also covers food and beverage, home care, health and beauty products.

For FY10 ended Dec 31, Zhulian chalked up a 6.2% grwoth in net profit to RM87.07 million, on the back of a 2.3% growth in revenue to RM322.61 million.

While the MLM business does depend on economic conditions, RHB Research’s analyst said even when economic growth was softer than expected, people may still look towards MLM for ancillary income.